User donetteeib02 uploaded the image

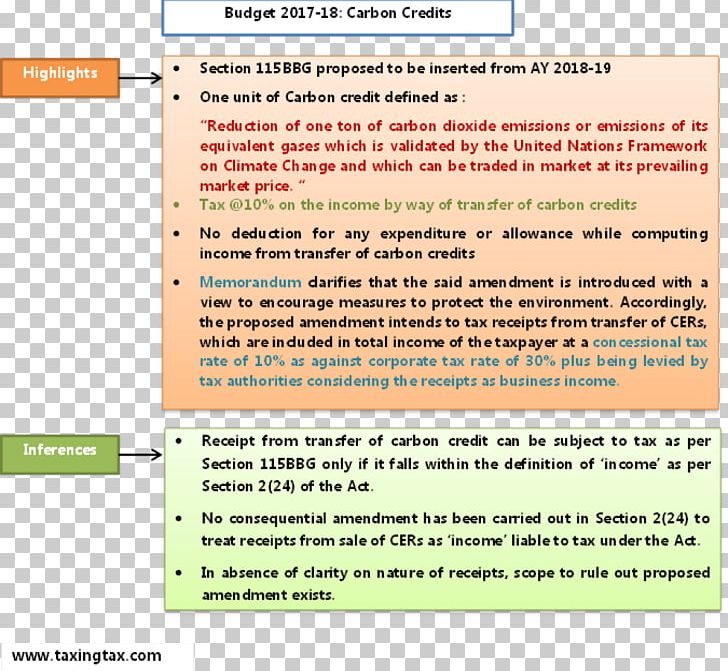

A screenshot of a document titled "Budget 2017-18: Carbon Credits". The document is divided into two sections. The top section is titled "Highlights" and has a title that reads "Section 115BBG proposed to be inserted from AY 2018-19". Below the title, there is a section titled "Reduction of one ton of carbon dioxide emissions or emissions of its equivalent gases which is validated by the United Nations Framework on Climate Change and which can be traded in the market at its prevailing market price". The bottom section of the document has a description of the proposed carbon credits, which states that no deduction for any expenditure or allowance while computing income from transfer of carbon credits is introduced with a Memorandum of Understanding (MEMORandum) to protect the environment. The document also mentions that the proposed amount of carbon tax is 30% less levied by tax authorities considering the receipts as business income. There is also a section labeled "Receipt from transfer to carbon credit can be subject to tax as per Section 111BBG only if it falls within the definition of income" and a section labelled "Section 2(24) of the Act". This section discusses the consequences of the carbon credit and how it can be carried out in Section 2 (24).

Income Tax Carbon Credit Budget Income Tax PNG

. The resolution of this PNG file is 978 x 906 pixels and it has a file size of 223.37 KB.A screenshot of a document titled "Budget 2017-18: Carbon Credits". The document is divided into two sections. The top section is titled "Highlights" and has a title that reads "Section 115BBG proposed to be inserted from AY 2018-19". Below the title, there is a section titled "Reduction of one ton of carbon dioxide emissions or emissions of its equivalent gases which is validated by the United Nations Framework on Climate Change and which can be traded in the market at its prevailing market price". The bottom section of the document has a description of the proposed carbon credits, which states that no deduction for any expenditure or allowance while computing income from transfer of carbon credits is introduced with a Memorandum of Understanding (MEMORandum) to protect the environment. The document also mentions that the proposed amount of carbon tax is 30% less levied by tax authorities considering the receipts as business income. There is also a section labeled "Receipt from transfer to carbon credit can be subject to tax as per Section 111BBG only if it falls within the definition of income" and a section labelled "Section 2(24) of the Act". This section discusses the consequences of the carbon credit and how it can be carried out in Section 2 (24).

You might also like...